港黃金清算系統開張!首日暴衝6676口打破紀錄-對抗西方紙市場,還是換個時區的同一套把戲?

2025年,全球金礦產量創下歷史新高,約3672噸。但漂亮數字的背後,藏著一個更關鍵的真相。這集我們要先把兩個常被混在一起的詞分清楚:

產量,是今年真的從地底下挖出來、變成金條的量。

儲量,是還埋在地底下、已經被探勘確認、未來才會開採的量。

產量是流量,儲量是存量。今年挖最多,不代表地底下還剩很多。真正的隱憂,藏在存量這一端。

本集帶你看懂黃金市場最被忽略的供給端:

🔹 儲量替代率跌破紅線:全球最大產金商,這一年開採掉約720萬盎司,但新探勘確認、登記進帳、未來才會挖的新儲量,只補進約200萬盎司,等於每挖1盎司只補回約0.28盎司。而且這補進來的,多半還是把舊礦重新分類,不是真的探到新金子。

注意,雖然黃金超過咗美債,但並冇超過美元計價嘅總資產,目前美元資產喺全球總儲備中嘅比例仍然以42 % 穩居第一,但其佔比已經跌破50 % ,為有記錄以來嘅最低水平。與此同時,全球央行嘅黃金總儲備已經突破3.6萬噸,逼近布雷頓森林體系嘅歷史顛覆值3.6萬噸。

雖然美元整體資產喺全球儲備中仍然以42 % 嘅份額穩居第一,但佢嘅佔比已經跌破57 % ,係有記錄以來最低。全球央行黃金儲備總量已經突破3.6萬噸,逼近布雷頓森林體系時期嘅歷史峰值3.8萬噸。半個多世紀以來,黃金喺世界貨幣體系中嘅地位正好走出咗一個「無往不復」嘅軌跡。

2026年4月1日,印度金融史迎來標誌性一刻 —— 印度儲備銀行( RBI )新規正式生效,白銀同黃金平起平坐,成為合法銀行抵押品,全面開啟國家級白銀貨幣化實驗。

截至5月下旬,政策落地僅1個多月,印度白銀抵押貸款已經從試點走向全民瘋搶,銀行爆單、萬億存量激活,疊加莫迪政府嚴控白銀進口嘅反向助推,呢場「越禁越火」嘅狂飆,正重塑印度金融邏輯,更改寫全球白銀格局。

一、白銀正式躋身 “ 準貨幣 ”

2025年10月, RBI 正式發布《金銀抵押借貸指引》,明確2026年4月1日起,白銀納入正規金融抵押體係,核心規則同黃金完全同權,並且暗藏強貨幣化設定。

新規劃定清晰邊界:僅接受銀飾、銀幣(唔接受銀條、工業銀),個人抵押上限為10公斤(黃金為1公斤);抵押率( LTV )分檔同黃金相同,25萬盧比以下貸款最高85 % ,25 – 50萬盧比80 % ,50萬盧比以上75 % ,25萬盧比以下無需信用審核即可放款。

即係話,如果一個人攞價值10萬盧比嘅銀飾辦抵押貸款,可以從銀行借到7.5萬盧比。呢個部分就係留畀貸款方嘅「風險冗餘」。

此外,政策覆蓋國有銀行、商業銀行、地區農村銀行、信用合作社以及非銀金融機構全面落地,徹底打破此前白銀僅喺民間私下抵押嘅灰色狀態,正式納入印度金融體系。

換言之,印度成為現代歷史上首個為白銀設定結構化貨幣基準嘅國家,並將佢視為同黃金平行嘅價值儲存方式。

二、市場爆發,複製黃金貸款狂飆路

政策落地後,印度白銀抵押貸款市場以遠超預期嘅速度爆發,成為繼黃金貸款後,印度最火熱嘅信貸賽道。

官方雖然未公布4月首月具體放款數據,但一線市場熱度已經無法忽視:大量農戶拎住銀飾銀幣上門抵押;各大銀行同非銀金融機構上千家網點首日上線,印度互聯網上出現唔少呢類網站⋯⋯

媒體預測,印度白銀抵押貸款首年規模將達到5000億盧比,到2028年將暴漲10倍,突破5萬億盧比,增速直接對標黃金貸款 —— 黃金貸款餘額從2021年唔夠1萬億盧比,飆升至2026年5月嘅4.6萬億盧比,已經遠超印度信用卡未償債務(3萬億盧比)!

三、8萬噸沉睡白銀被激活!

印度敢做白銀貨幣化實驗嘅底氣,來自天量嘅「沉睡白銀」。

據估計,印度民間持有7.5萬至8萬噸家庭白銀。僅過去五年,印度消費者,尤其係收入較低嘅農村群體,就累計購買咗約29000噸銀飾同4000噸銀幣!

規模咁巨大嘅白銀實物,大部分被鎖喺首飾盒入面。就算只有一小部分進入正規金融體系,都會改善市場流動性,促進經濟發展!

而莫迪政府嘅進口限制,更係火上澆油。 2026年5月,為保衛盧比、節約外匯,印度將金銀進口關稅由6 % 上調至15 % ,隨後直接將銀條、半成品白銀納入限制進口目錄(佔印度白銀進口總量嘅90 % 以上)。

呢一系列操作導致國內白銀供應收緊、價格上漲。截至5月18日,國際銀價單月上漲4 % ,而印度國內銀價上漲咗10 % !

民間惜售情緒高漲,更願意通過抵押換取現金 —— 既解決資金需求,又保留資產所有權,避免高價買返嘅成本。

盧比持續貶值、通脹高企,銀行收緊無擔保貸款額度,只認實物抵押。黃金多集中喺中高收入家庭,而抵押白銀係部分印度農民避開高利貸、快速融資嘅唯一出路。

四、白銀抵押貸款係銀行嘅「必爭之地」

對印度金融機構嚟講,白銀抵押貸款係完美業務,低風險、高收益、需求旺盛,係經濟寒冬中嘅「避風港」。

呢類貸款嘅優勢一目瞭然:實物白銀(飾品、銀幣)喺手,壞賬率遠低於無擔保貸款;利率喺10 % 到24 % ,高於普通貸款,利潤空間充足;獲客成本極低,民眾主動上門,無需大規模營銷;政策加持,央行鼓勵擴張,監管規則清晰。

喺印度經濟遭遇中東戰事,前景同唔確定性明顯增強。 5月19日,國際貨幣基金組織( IMF )嘅《世界經濟展望》認為,隨住匯率暴跌,印度名義 GDP 略高於4萬億美元,已經被日本同英國反超,重新降返全球第六大經濟體。高盛曾經預測印度2026年經濟增速將超過7 % ,但近期已經兩次下調預期,下調至5.9 % 。

喺無擔保貸款被央行嚴控,而且嚴格禁止暴力催收嘅背景下,白銀抵押貸款業務當然會被積極推進。

五、各種實際問題仍然喺度解決

到目前為止,金融機構仲未有詳細嘅鑑定、估值、倉儲同拍賣流程嘅標準化操作規程。檢測黃金,填寫文件,放出貸款通常只需15-20分鐘,但白銀唔得。

對白銀嘅估值,必須基於實際純度,參考 IBJA (印度金銀協會)或 MCX (印度多種商品交易所)嘅牌價按成色調整。但白銀飾品同銀幣唔係標準化產品,行業內冇公認嘅、簡單嘅方法嚟測試含銀量。

呢個係白銀抵押貸款擴張規模嘅最大障礙。

印度民間嘅白銀存量雖然大,但係年代、品質參差唔齊,大多數銀飾純度並唔高,通常喺60-70 % 之間,有時甚至更低。某啲古代銀幣含銀量只有8 % ,極其難以估值。

大多數銀器比較厚,結構仲複雜,只檢測表面含銀量嘅風險巨大,切開檢測亦唔現實。

喺印度全國數千個做白銀抵押貸款嘅網點部署 X 射線熒光光譜設備( XRF )有極大困難。而且印度嘅白銀製品成分唔均勻,有時測試幾個點,白銀含量都唔一樣。有時仲要用電導率、超聲波同密度測試⋯⋯

客戶提供嘅銀飾發票上嘅含銀量,往往同測試結果有巨大差異。

噉就造成金融機構畀白銀製品估值,經常變成同客戶嘅激烈爭吵。目前業內普遍認為,啱啱開始唔好碰複雜嘅銀飾,主攻更標準化嘅銀幣,先可以避免出現壞賬嘅風險。

六、白銀嘅貨幣化實驗啱啱開始

對印度嚟講,白銀抵押貸款一舉三得:激活沉睡資產,為農村低收入群體提供低成本融資渠道,緩解信貸失衡,增加全社會嘅流動性。

對全球白銀市場嚟講,印度嘅貨幣化實驗更加係顛覆性嘅。白銀從工業金屬(光伏、新能源、芯片核心材料),升級為「工業 + 避險 + 準貨幣」三重屬性資產,而且會喺印度重新放開管制後,進一步增加白銀需求!

印度呢場國家級白銀貨幣化實驗嘅走向,唔單止會影響印度金融嘅未來,更會深刻影響全球白銀格局同貴金屬定價邏輯。等我哋繼續仔細觀察!

宋鴻兵

🇨🇳CHINA PULLED ITS SILVER RESERVE FROM GLOBAL MARKETS⚠️ -Alasdair Macleod

🚨US DECISION TO CLASSIFY SILVER AS A CRITICAL MINERAL TRIGGERED CHINA TO URGENTLY CHANGE ITS GAME PLAN:

youtube.com/watch?v=PcvXSZ…

這張圖乍看很簡單,卻很震撼。很多人一提到印鈔,就先想到美國,但把中國與美國貨幣供給放在一起比較,會發現中國的擴張幅度其實更驚人。

從圖上可以看到,2009年前後中國貨幣供給正式超越美國,之後一路快速拉開差距,到2026年已超過5兆美元級距,明顯來到美國的兩倍以上。

這代表中國過去十多年的成長,背後不只是生產力提升或勤奮工作,更大一部分其實來自債務驅動,再透過持續擴張貨幣,把成長撐出來。

換句話說,所謂每年約5%的GDP成長,很多時候不是自然長出來的,而是用更多信用、更多負債、更多流動性,一層一層堆出來的結果。

這也解釋了另一個問題,為什麼中國需要持續增加黃金配置。因為如果貨幣供給一直膨脹,單靠少量買金,根本不足以提升人民幣的市場信任。

更直白地說,如果中國想讓人民幣更有信用,黃金購買速度不只要增加,甚至必須跑贏印鈔速度,否則只是帳面好看,無法真正改變貨幣基礎。

而這張圖真正揭露的,還不只中國。無論是美國、歐洲還是中國,現代經濟系統本質上都建立在債務擴張與新貨幣投放之上,只是速度與規模不同。

https://www.facebook.com/share/p/18bn6F2V6k/?mibextid=wwXIfr

隨著中東緊張局勢持續升級——美伊衝突加劇、霍爾木茲海峽面臨威脅——中國為進口伊朗石油搭建的隱密金融基礎設施,再度引發關注。這項繞開美元的支付與資產循環體系,不僅幫助伊朗維持了石油出口(中國目前吸收了伊朗超過八成海運原油),也穩步推進了北京的去美元化戰略。

本期快訊基於多方可靠資訊及近期地緣政治動態,拆解從結算到黃金轉換的完整機制鏈。

---

1. 核心結算通道:崑崙銀行

崑崙銀行,由中國石油天然氣集團公司(中石油)控股的中小型商業銀行,已成為中伊石油貿易結算的主通路。

· 核心角色:處理超過90%的中伊石油交易,全部以人民幣結算,完全繞過美元體系。

· 規避制裁:崑崙銀行針對伊朗業務建立了一套封閉的人民幣結算循環,與SWIFT系統完全隔離。美國早在2012年就對其施加製裁,切斷了其美元清算通道,這反而使該行成為高風險、非美元貿易的理想結算工具。

· 運作方式:伊朗原油常透過「暗池船隊」(關閉AIS訊號)偽裝成馬來西亞來源運抵中國。中國買家(多為獨立民營「茶壺」煉廠)透過崑崙銀行以人民幣支付,伊朗則在崑崙銀行取得人民幣帳戶額度。

· 「資金沉澱」現象:受制裁限制,這部分人民幣既難以兌換成美元,也無法自由匯出伊朗。伊朗雖用部分資金進口中國商品(機械、電子產品、基礎建設等),但大量盈餘長期以「未來交付中國商品的義務」形式沉澱在崑崙銀行的伊朗帳戶中,實質上形成了封閉運行的人民幣餘額。

這個循環讓中國能以低於市價的價格進口伊朗原油(通常每桶比基準價便宜8–10美元以上),而伊朗則在被制裁的困境中保住了出口收入。 2025年,中國從伊朗日均進口原油約138萬桶,佔其海運進口總量的13.4%。

---

2. 資金出口:上海黃金交易所的整合

盤活沉澱人民幣的關鍵,在於全球最大的實體黃金交易平台-上海黃金交易所。

· 人民幣轉黃金:伊朗(或其關聯實體)可將累積的人民幣透過上海黃金交易所購入實體黃金。該交易所強調實物交割,買方可以從指定金庫提取純度達99.99%以上的金條。

· 透過境內帳戶實現低可識別度操作:為了降低被關注和製裁的風險,這些購買往往透過上海黃金交易所的「國內主機板」帳戶進行,而非專為境外參與者設立的「國際板」。國內帳戶原本主要服務境內機構,隱蔽性更高——可以透過中國境內中介或關聯方間接操作,避免直接以境外實體的身份登記,從而進一步隱藏資金與石油收入的關聯。

· 國際板作為補充:境外參與者也可以透過國際板(SGEI)進行人民幣計價的黃金交易。近年來,隨著香港等地離岸金庫的佈局以及共同託管安排的討論,未來受制裁實體在黃金存儲和流動上可能有更多靈活選項。

· 戰略價值:將「沉澱」的人民幣轉化為便於攜帶、抗制裁的硬資產。即伊朗賣油 → 收入人民幣 → 購買上海黃金交易所的黃金(常透過境內管道隱藏操作)→ 持有或運回黃金作為儲備或避險資產。這條路徑為伊朗提供了進口中國商品以外的新選擇,增加了其資金運用的彈性。

· 更廣泛影響:此機制強化了人民幣國際化(借助「上海金」定價基準),也契合中國推動人民幣在大宗商品貿易中使用的目標。在金磚國家及海灣合作委員會框架下,透過提供可靠、可兌換黃金的“出口”,有利於鼓勵石油出口國接受人民幣結算。

分析師認為,如果將伊朗及海灣國家的美元石油貿易與離岸黃金託管安排相結合,在中東局勢緊張的背景下,可以建構「石油人民幣—石油黃金」的轉換路徑。

---

3. 地緣政治背景與2026年3月最新動態

目前油價在地緣衝突中波動於70–100美元/桶區間。

· 據伊朗官員及多方報道,伊朗正與多國商討,以採用人民幣計價石油為條件,換取霍爾木茲海峽通行保障。

· 此舉直指石油美元的主導地位,考慮到全球約20%的原油運輸需經過霍爾木茲海峽,其戰略意義不言而喻。

· 中國也持續增加黃金儲備(截至2025年底約2,306噸),並積極推動人民幣能源定價(如可兌換黃金的原油期貨),進一步鞏固了此體系的根基。

此機制的韌性較強:崑崙銀行本就遊離於美元體系之外,西方進一步製裁的施壓空間有限;上海黃金交易所則提供了穩定的資金循環通道,尤其是透過境內帳戶的隱藏操作,增加了系統的抗干擾能力。

---

總結

中伊之間「人民幣結算—石油交易—黃金轉換」的循環——透過崑崙銀行完成資金清算,再經由上海黃金交易所(常以境內帳戶形式隱蔽操作)轉化為黃金——形成了一套在製裁背景下切實運行的去美元化能源貿易模式。這套模式為中國帶來了價格優惠的石油,為伊朗保住了關鍵的出口收入,並透過實體資產的流動,逐步對美元霸權形成實質削弱。

隨著中東局勢不斷演變,人民幣與黃金連動機制是否會進一步製度化,值得持續關注。這並非理論推演,而是一個正在運作並不斷擴展的現實。

請留意能源與金融交會領域的最新動向。

2月26日(路透社)—印度市場監管機構週四指示,自2026年4月1日起,共同基金應使用國內證券交易所的現貨價格來評估其持有的實體黃金和白銀。

印度證券交易委員會(SEBI)表示,共同基金現在可以使用來自認可的證券交易所的現貨價格,這些交易所結算實物交割的黃金和白銀衍生品合約,以確保估值反映國內市場狀況。

此次變更將不再使用倫敦金銀市場協會(LBMA)的價格來評估交易所交易基金(ETF)持有的黃金和白銀。

現在的世界是一個高風險的世界。金融、社會、戰爭它們之間 是三位一體的關係,牽一髮而動全身。而造成這個高風結構的罪魁禍首,就是萬惡的國家紙幣系統,以及躲在紙幣系統背後的中央銀行、政府和金融機構。

億萬投資者 Ray Dalio 喺 2026 年 2 月 9 日訪問中警告:央行數碼貨幣(CBDC)即將來臨,會消除金融私隱,畀政府權力即時稅收、沒收資金同切斷政治對手嘅資金來源。

- Dalio 作為 Bridgewater Associates 創辦人,

- 帖文引發加密社群熱議,回復多推廣私隱幣如 Zcash 同 Monero,視為對抗 CBDC 監控嘅替代方案,反映 crypto 界對金融自由嘅關注。

TL; DR

Authored by GoldFix

Housekeeping: Presented two ways: Accessible podcast (on site) , and slightly more formal written version below. What looks like a debate about Stablecoin vs. CBDC is really a global struggle for control

“Payment is a monetary supply chain. The world is now contesting that chain, with the U.S. defending the dollar and China advancing the yuan. Gold appreciates inside this conflict as the only truly global settlement asset both sides can use.”

The global debate over stablecoins, central bank digital currencies, and BRICS monetary initiatives is widely misunderstood because it is framed through technical jargon rather than power, control, and incentive structures. At the macro level, stablecoins and CBDCs are policy tools. At the geopolitical level, they are weapons in a contest between a challenged reserve currency and a rising multipolar order. At the secular level, they reflect a return to mercantilism, where nations compete to control payment rails, capital bases, and settlement mechanisms. The fight is not about technology. It is about who controls money, where it circulates, and whose rules govern trade.

The current monetary discourse is saturated with overlapping and often contradictory language. Stablecoins, CBDCs, tokenized money, digital rails, programmable currency. The terminology itself obscures the underlying dynamics.

“If this soup of terminology is seemingly confusing, well, if you take a look at it from a macroeconomic perspective it will make sense. But if you take a look at it from a geopolitical, secular perspective, a mercantile perspective, it makes a lot more sense.”

The confusion is not accidental. Much of the debate focuses on surface-level mechanics while avoiding the structural motivations behind policy choices. When framed properly, the behavior of the United States, China, and the BRICS bloc follows a coherent logic.

At the macroeconomic level, the discussion centers on rules, policies, and official justifications. Governments explain their actions in terms of consumer protection, financial stability, and monetary sovereignty.

From this vantage point, the United States seeks to maintain its position as issuer of the global reserve currency. One adaptation under consideration is the expansion of dollar-based stablecoins. These instruments allow the dollar to move more easily across borders and into jurisdictions where direct dollarization would face resistance.

“Stablecoins are a sugar-coated wrapper that makes it easier to swallow the bitter pill of U.S. dollar dependency, especially for smaller countries.”

In response, many nations either ban stablecoins outright or restrict them unless issued under domestic authority. The stated solution is the adoption of central bank digital currencies, which are framed as tools to protect citizens and preserve national monetary systems.

At this level, the narrative appears fragmented. Some countries ban stablecoins. Others encourage them. Some experiment with CBDCs. Others delay. Taken only at face value, the policy landscape looks inconsistent.

Zooming out reveals coherence. What appears fragmented at the policy level resolves into a contest between two opposing monetary objectives.

On one side stands the incumbent global reserve currency. On the other stands a coalition seeking multipolarity.

“What the BRICS are really doing by banning stablecoins and adopting CBDCs is shutting the dollar out. They want their currencies to float economically and discover their own value.”

BRICS initiatives such as cross-border settlement platforms, bilateral trade arrangements, and large-scale gold accumulation are not isolated projects. They are components of a broader strategy to reduce reliance on the dollar-centered system.

This shift places the dollar on the defensive. Stablecoins become a countermeasure. They allow the dollar to retain relevance even as formal banking and settlement channels fragment.

“It is BRICS versus the United States. Multipolarity trying to assert itself and the incumbent reserve currency trying to protect its position.”

At this layer, stablecoins and CBDCs cease to be neutral technologies. They become instruments of strategic competition.

Zooming out again reveals the deepest framework. The global economy is transitioning away from globalism toward regionalization. As trade blocs harden, so do monetary zones.

“The world is split in two. The world is regional. And as a regional world breaks down from globalism, you are going to have regional currencies.”

In such a system, nations prioritize control over capital flows, tax bases, and internal demand. This is mercantilism in modern form. Digital money simply accelerates and formalizes the process.

China’s opposition to stablecoins follows directly from this logic. Dollar-linked stablecoins represent an injection of foreign monetary influence into the domestic economy.

“To use dollars at the retail level is to replace the currency of the nation slowly and surely from the inside out.”

CBDCs, by contrast, lock capital within national systems. They reinforce domestic control while enabling selective engagement externally.

The United States approaches the problem from the opposite position. As the dominant issuer, it benefits from global circulation of its currency. If traditional mechanisms weaken, alternatives must be developed.

“If the U.S. cannot maintain its global reach with its currency as it currently stands, then it needs to adapt to what BRICS are doing.”

Stablecoins become the adaptation layer. Even without adopting a formal CBDC, stablecoins can replicate many of the same control functions domestically while preserving private-sector intermediaries.

“Stablecoins will serve the same purpose as CBDCs for U.S. citizens, just run by private companies. And there’s your corporatism.”

As mercantilism reasserts itself, money bifurcates by function.

Domestically, nations deploy digital currencies to manage taxation, compliance, and internal stability. Internationally, different instruments emerge to settle trade and sovereign obligations.

“You are going to have money that you use to buy things, and then you are going to have money that you use to settle international debts.”

In parts of the East, this may involve CBDCs paired with gold-linked settlement mechanisms. In the West, it may involve stablecoins layered atop existing financial infrastructure.

This division mirrors historical mercantilist systems where trade settlement and domestic circulation operated under different rules.

At the core of this entire transition lies one concept.

“Payment rails are the things that people use to settle their trades.”

Payment rails determine whose currency is used, whose rules apply, and whose system captures transaction data and fees. They are fragmenting globally.

https://x.com/tavicosta/status/2019866206807945228?s=46&t=rt3XmYmqG_eB8lRu6xQtZg

這種情況前所未有。

而且,這並非黃金獨有的現象。

大多數金屬的重大新發現數量都已降至個位數,目前沒有任何具有實質改變全球供應曲線的在建項目。

這才是衡量我們目前所處礦業週期階段的真正晴雨表。

現在還處於早期階段。

2011年9月9日晚上11點01分,一封看似普通的電郵被發送到Jeffrey Epstein(中文常譯為「傑弗里·愛潑斯坦」)的私人郵箱 jeevacation@gmail.com。寄件人身分目前仍被部分遮蓋,但內容卻直白得令人震驚:

「我們應該研究一下這種可能性,以及如果中國決定放棄貨幣與美元的掛鉤,改用黃金作為替代,該如何從中賺錢。」

這句話出自13年前,當時全球金融市場仍處於2008年金融海嘯後的餘波,美元作為世界儲備貨幣的地位看似牢不可破,人民幣對美元的「盯住式」匯率機制(俗稱「盯住美元」或「美元掛鉤」)也仍是中國外匯政策的核心支柱。誰能想到,一個以性犯罪醜聞聞名的金融圈人物,竟在私下討論如此宏觀且具顛覆性的地緣貨幣議題?

背景:2011年的中美貨幣博弈

2011年,中國已是全球第二大經濟體,持有超過3萬億美元的外匯儲備,其中大部分是美國國債。人民幣匯率長期被美國指責「人為低估」,中美之間的「貨幣戰」爭論不休。同一時期,黃金價格正處於歷史高位(2011年9月金價一度衝上1,900美元/盎司以上),不少投資者已開始質疑美元的長期信用。

愛潑斯坦這封電郵的時間點非常微妙:

他不是在談道德或地緣政治,而是赤裸裸地問:「如果中國真的這麼做,我們怎麼賺錢?」

這封電郵意味什麼?

結語:歷史總在重演,只是參與者換了面孔

今天我們看到的是:央行拋售美債、增持黃金、數位貨幣試點、跨境黃金結算……這些動作,早在13年前就有人在私下盤算「怎麼賺錢」。當全球貨幣秩序真的走向轉型時,那些最早看到方向的人,往往已默默完成布局。

愛潑斯坦或許因罪行身敗名裂,但這封電郵卻意外成為一個時代註腳:

當權力、金錢與地緣政治交織時,有人永遠在問同一個問題——「我們怎麼從中賺錢?」

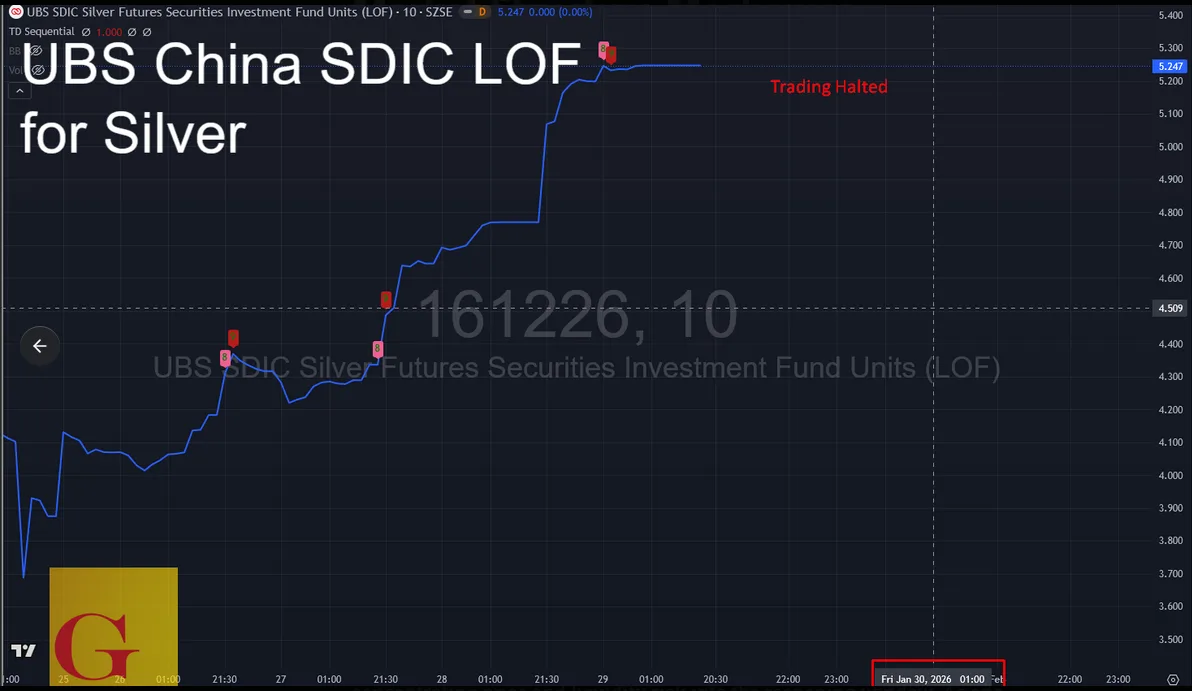

GFN – SHANGHAI

Trading in a major China-listed silver fund was halted for a full session on January 30 as regulators moved to contain price distortions, while global silver prices fell sharply from record highs amid elevated volatility and tighter derivatives margin requirements.

China’s Shenzhen Stock Exchange suspended trading for the entire day on January 30 in the UBS SDIC Silver Futures Fund LOF, according to an official fund announcement. The notice stated that trading would be halted from the market open through the close as part of exchange risk-control measures.

“该基金将于2026年1月30日开市起停牌至收市。”

(“The fund will be suspended from market open to market close on January 30, 2026.”)

— SDIC Silver LOF official announcement, cited by Sina Finance

Chinese financial media reported that the halt followed sustained abnormal trading conditions, with the fund’s secondary-market price diverging materially from its net asset value. Coverage described the suspension as a regulatory response to excessive premiums and repeated risk warnings rather than a change in the underlying structure of the fund.

At the same time, silver prices in international markets recorded one of their largest single-day declines after reaching historic highs earlier in the week. Reuters reported a sharp reversal across precious metals during the January 30 session.

“Gold, silver and copper prices dropped sharply on Friday… Silver dropped 11% to $103.40, after peaking at $121.60.”

— Reuters, Metals Markets Wrap, January 30

Market data showed extreme intraday volatility, with spot silver falling back toward the $100 per ounce level after touching record highs the prior day.

Derivatives market conditions also tightened during the period. CME Group confirmed that it had raised margin requirements on silver futures contracts in response to heightened volatility and rapidly rising prices earlier in January.

“Margins will rise to 11% of notional from the current 9% for non-heightened risk profiles, while heightened risk profile margins will be raised to 12.1%.”

— CME Group margin notice, reported by Mining.com

CME described the changes as routine risk-management adjustments designed to ensure orderly market functioning during periods of exceptional price movement.

The January 30 session combined regulatory intervention in China-listed commodity funds, sharp price corrections in global silver markets, and tighter derivatives margin conditions, all occurring after a rapid, record-setting rally in precious metals earlier in the month.

Market participants familiar with exchange-traded commodity products and futures market plumbing highlighted several structural effects stemming from the January 30 fund halt, emphasizing mechanics.

First, industry professionals noted that halting a fund while the underlying commodity continues to trade materially increases risk for fund holders. Traders pointed out that the absence of secondary-market pricing during the session removed the ability of the UBS trader to manage exposure dynamically, concentrating price and liquidity risk into the reopening window. As one derivatives trader put it, the halt “freezes the wrapper, not the asset,” leaving holders exposed to NAV moves they cannot respond to in real time.

Second, sources close to ETF and LOF operations said that such halts interrupt speculative momentum within the fund vehicle itself, particularly when the product has been trading at a significant premium to NAV. By suspending trading, (risk/pseudo) arbitrage and momentum flows are paused, and reopening typically forces a reconciliation between NAV, secondary-market pricing, and redemption demand. Market professionals stressed that this process often reduces speculative excess in the fund, even if it does not alter the underlying commodity’s physical supply and demand.

Third, traders active in futures markets emphasized that freezing the fund while leaving futures markets open can shift adjustment pressure elsewhere. With the fund temporarily non-redeemable, price discovery and risk transfer continue primarily through futures and related derivatives. Several participants noted that this dynamic can accelerate position adjustments in leveraged futures accounts, particularly when margin requirements are rising and volatility remains elevated. But it still does not guarantee the LOF will shrink its NAV premium

One seasoned trader close to the action speculated:

This fund will likely go the way of all funds like PSLV that attract interest.. it will be castrated financially. You are witnessing a stealth global capital control on Silver. Best you not use derivatives.

That trader concluded with: If you want to own silver.. Buy physical. A bird in your hand is worth 2 in the bush.

Taken together, and assuming the facts reported are true, industry participants characterize the January 30 actions as possibly necessary from a market-order perspective to bring the fund back toward reasonable trading levels as China’s primary silver exposure vehicle, but structurally asymmetric in execution. By halting the fund while futures markets remained fully active, the adjustment burden was deferred and displaced rather than resolved. The fund’s premium may or may not have been reduced upon reopening com Monday, but during the session itself the broader silver market absorbed the pressure, contributing to a disorderly unwind of leveraged long positions in futures and related instruments.

While communication among international exchanges during periods of stress would not be surprising, the outcome was clear: the market was managed inefficiently in pursuit of fund-level stability, transferring stress outward into global futures markets. If nothing else, the episode reinforces a point long argued by GoldFix since 2023: the Shanghai price is now the global price and that physical is king.