Silver has been rising in Russia only as a hedge against the government

This could be a major turn of events that will have global implications. The action’s set to unfold in Mexico, where many of its most influential and wealthy citizens are demanding the country abandon its fiat currency, the Peso, and return to a silver standard. … We know that many people are used to looking at Mexico as the violent, crooked, messed up country over the border… the one that sends all those illegals over here because even picking canteloupes for giant U.S. agri-businesses pays better than the job at home… it’s now time to rethink all that, because a silver standard in Mexico would unleash the biggest global power shift since Spain raided the Aztecs 600 years ago. It’s unavoidable. History repeats itself, especially when its exactly the same economic situation.

http://demonocracy.info/infographics/world/silver/silver.html |

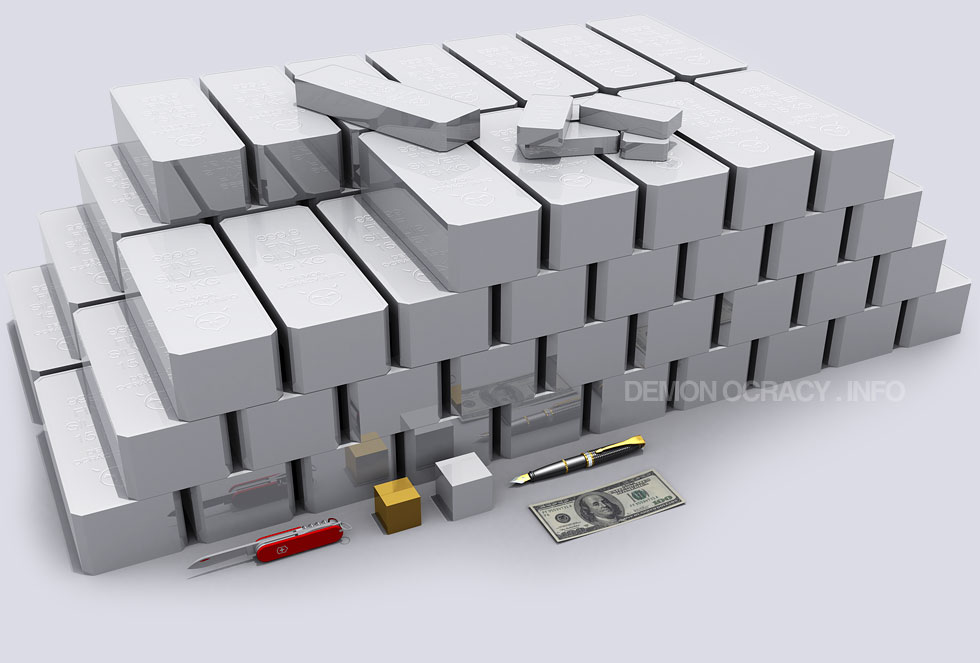

| Silver – Size Chart |

| This is a chart of standard Silver bullion size comparison. The silver bars are measured by Silver volume & weight of 10.49 g/cm−3 in typical Silver Bar Dimensions. |

| 1 Ton of Silver = $1 Million @ $31.10 / Troy oz |

| Silver price is hovering around $30/ troy oz, once Silver hits $31.10 / troy oz, Silver will cost exactly $1/gram, at that point the 1 Ton of Silver displayed above will be worth exactly $1 Million DollarsSilver is not purposely mined, 80% of new Silver production is a by-product of Gold or Copper mining, this is due to Silver’s recent low value compared to other metals. Silver has the best electrical conductivity of any element and highest thermal conductivity of any metal.  1 Ton of Silver 10 Tonnes of Silver 100 Tonnes of Silver 1000 Tonnes of Silver The 1 ton of silver is worth $1 million dollars at $31.10 / troy oz. While there are significant Silver reserves underground, due to the low prices they are not being mined. Silver has run a 63 year long supply/demand deficit as of year-end 2004, this is mainly due to Silver getting lost and industrial production demand, including x-rays, photography, mirrors, electrical and electronic products. This amounts to a deficit of 331.46 Tonnes since 1942. Source |

| ||

| Silver Bar |

| |

| Silver Bar |

| |

| 人民幣 |

|

| Gold Bar |

|

| Gold Bar |

Substantial production losses and outages at existing copper mines will cause global copper inventories this year to fall to 47 days of consumption from 52 last year, Scotiabank economist Patricia Mohr has forecast.——————————–

While refined copper stocks average 61.1 days of consumption from 2000-2009, “LME inventories have actually declined in 2012 and overall global inventories are expected to fall to 47 days of consumption from 52 last year, despite the recent increase in bonded warehouse stocks in China,” said Mohr. “This reflects substantial production losses & outages at existing mines this year-Escondida (Chile -75,000 tonnes), Collahuasi (Chile), Los Bronces (Chile -60,000 tonnes), Grasberg (Indonesia -100,000 tonnes) and Lumwana (Zambia -60,000 tonnes).”

“Major Canadian gold miners are also examining project expansion more critically, in part due to high capital cost inflation,” she added.———————–

Recent announcements by BHP Billiton of project delays, “reflect concern over capital-cost escalation in the face of more subdued metals prices,” Mohr advised. “In copper, capital cost inflation (which normally lags metals prices) has averaged 22% per annum from 2002-2011 and is projected to increase by 15-20% this year.”

A prominent PBOC Advisor has stated that US Treasuries are not safe in the medium to long term, and has recommended China increase it’s gold reserves as well as add silver to it’s official reserves.

A prominent PBOC Advisor has stated that US Treasuries are not safe in the medium to long term, and has recommended China increase it’s gold reserves as well as add silver to it’s official reserves.“People like me who have tremendous confidence in silver and are invested in the market see it rising once the easing begins,” said Jeffrey Sica, the Morristown, New Jersey-based president of SICA Wealth Management, who helps oversee about $1 billion of assets. “I expect an acceleration in the fear trade. Most of the hedge funds who sold will be back once the market gathers momentum.”