馬田大師

The chaos in gold is typical. Already, the hate mail has begun.

“Stop the Bullshit”

one said because demand in Shanghai is at record highs.It takes far

more than one country to make a bull market. Others just blame me for

the decline because they just listen to those who always say buy. The

New York institutional press would

NEVER dare quote me

because I stand up and expose their favorite sons – the NY bankers. The

Goldbugs do their best to make sure their press does not quote me since

they only have a litany of people who say

buy – buy – buy! So why is it always me?

People are so married to this idea of the entire world collapsing and

only gold will rise it is truly astonishing. What is the problem? Why

must gold be the exception to everything? This is not a religion. It is a

market. I hate to tell you but everything on a timing level was on the

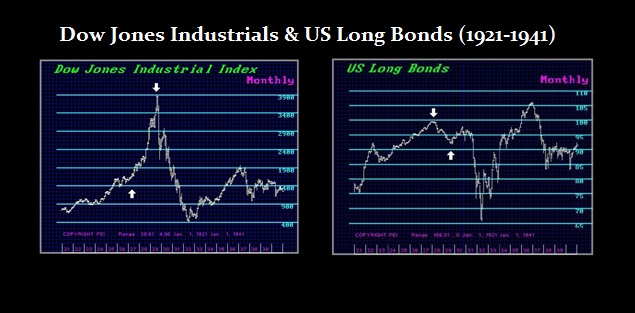

mark. The collapse in the stock market during the Great Depression was

34 months. The rally in gold was 34 months. These are reoccurring timing

frequencies in times of crisis. This is about making money and

surviving – not punishing the world because you are not on the top of

the food chain. I am not selling anything. I am not soliciting funds for

management. It always is what it is. Nothing more!

People have been sold pure nonsense on so many fronts. The talking

heads claim lower interest rates are bullish for stocks. Just do the

correlation and you will see that when rates plummet as during the Great

Depression or after 2007, stocks fell. So precisely where does this

nonsense emerge? Who writes this bullshit for the talking heads?

The precious-metals investors have been sold the similar nonsense –

all hype and no substance that gold will rise because the Fed increases

the money supply. A very simple one-dimensional relationship that

NEVER works because we live in a

DYNAMIC world economy. Bull markets

ONLY take place when that object is rising in terms of

ALL

currencies. They have also been sold the nonsense that gold rises with

inflation. That was a great sales pitch, but it is time to do the

REAL

correlation. When you do the analysis rather than preaching dogma and

chanting mantras laced with rhetoric, strangely what emerges is

NOT that gold rallies with inflation, but it rallies when people

DO NOT TRUST the government! Just do the correlation and you may be surprised.

The release of the January meeting minutes of the Federal Reserve’s

policy committee show that members of the Fed were concerned that it

might be hard to reel in all this liquidity. Keep in mind, that very

concern assumes power to reverse such trends. Even Herbert Hoover point

out in his memoirs that proved to be yet another false assumption. The

Fed policy committee recognized that the liquidity itself may end up

contributing to instability in financial markets. Why? They see the Dow

off to test the 2007 highs. They are afraid there could be a bubble, yet

at the same time they are confronted by a contracting economy. They are

clueless as to what is going on. When asked what was their contingency

plan in case the Euro broke apart, they said that would never happen so

there was no plan. That is like putting up a building without fire exits

because you clearly had no intention of setting the building on fire.

Consequently, the irony confronting the precious-metals investors is

that this may mean the Fed will curb its expansionary monetary policy

SOONER than expected. Thus, gold plummeted for the sales pitch became the mover in reverse – buy for inflation, sell for deflation.

This may be the fundamental that shakes the weak longs out of the

tree, and melts the icing off the cake. Nonetheless, it is

just rhetoric. Gold will rise

NOT because of hyperinflation that will

NEVER take place. Gold will rise as the

Sovereign Debt Crisis unfolds. Understanding the difference prevents losses like today.

It is

NOT the inflation that we need to be concerned with long-term, it is the implosion of

DEFLATION. Unfortunately, when you are in a

Sovereign Debt Crisis

as took place in 1931, capital contracts and hoards because people are

confused and they will spend barely nothing until the sort out what is

really unfolding.

Gold will rise

NOT because of hyperinflation, but because of the

Sovereign Debt Crisis and the lack of a place to put money. The dollar is rising because you have

NO

place to put big money. Europe has no federal bond issue. Japan is a

basket case, and China has no bond market of any size. Thus, the US bond

market remains it. This is why 30 year mortgages have just dropped

below 4% and banks are now trying to lend mortgages as they see

liquidity increase (not from the Fed but capital inflows).

It is so important to understand the global fundamentals for

NO market, not even gold, is ever driven by a single fundamental or a single country. It is at all times a global affair.

Armstrongeconomics.com